Private fleets have thus far been driving Class 8 truck orders and have been taking more freight in-house to avoid supply chain disruptions they experienced after the pandemic.

However, competition from private fleets appears to be easing, ACT Research reports.

Competition from private fleets easing: ACT

ACT Research reported this week that its For-Hire Trucking Index continues to point toward a slowly recovering for-hire trucking market.

“Evidence and anecdotes suggest private fleets have taken some volume from the for-hire market,” said Carter Vieth, research analyst with ACT. “Given private fleets’ cost disadvantage, and lack of incentive for backhauls, we don’t expect this to last long, and recent Class 8 data suggests private fleet capacity additions are slowing, a welcome sign after an extended downturn.”

ACT’s Capacity Index decreased three points in April, a welcome sign for for-hire carriers.

However, volumes also decreased in April.

“While private fleet competition has weighed on volumes the past few months, it’s not likely to last long,” said Vieth. “Solid performance of rates and the load/truck ratio in the spot market through Roadcheck suggest the gradually improving volume trends will support the market balance in 2024. Overall, the supply-demand balance suggests a market close to the elusive and impermanent equilibrium.”

Shipper conditions improve slightly

Shippers saw a modest improvement in conditions in March, according to FTR, but conditions are set to deteriorate.

FTR’s Shippers Conditions Index improved in March, back to positive territory at 1.2 from -1.4 in February. Stable diesel prices and a slightly more favorable rates were to thank for the improvement.

“The SCI returned to mildly positive territory in March after February’s negative reading that mostly was due to fuel costs,” said Avery Vise, FTR’s vice-president of trucking.

“The next couple of months still look favorable for shippers, but we expect the index to trend toward more neutral and slightly negative readings by the second half of this year due to modestly stronger capacity utilization and less favorable rates. Even so, we expect any weakness in shippers’ market conditions over the next couple of years to be far milder than what they had encountered from late 2020 through the middle of 2022.”

{kind=link}

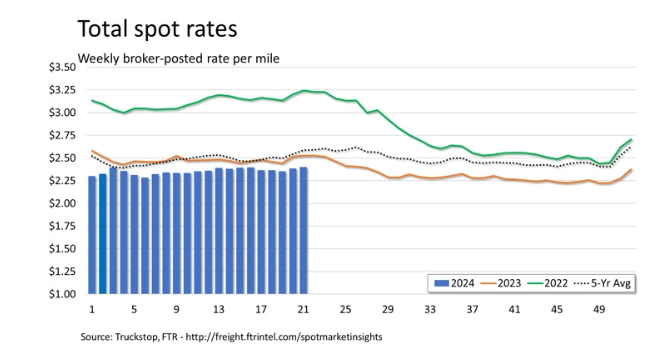

Spot market’s Roadcheck bump could have staying power

Truckstop and FTR Transportation Intelligence saw an increased improvement in spot market rates for the week ended May 24, suggesting the much anticipated Roadcheck bump could have some staying power.

This isn’t uncommon. Truckstop reports rate increases for the week following Roadcheck have occurred every year since the event moved to May in 2021.

“After significant gains in four of the past five weeks, spot rates for refrigerated van equipment barely exceeded those for flatbed equipment – for the first time since the fourth week of this year. Spot rates for van equipment are tracking more closely with comparable 2023 weeks than are rates for flatbed, which – while stable – have not shown any signs of their usual spring peak,” the companies said in a release.

“With a decline in load postings and an increase in truck postings, the Market Demand Index declined to 81.2. While lower than in the prior week, the MDI in the latest week otherwise was the strongest since the first week of 2023.”