The first look at the dealmaking environment for venture capital in the second quarter of 2024 revealed continued struggle, according to Pitchbook and the National Venture Capital Association.

The lead VC analyst Kyle Sanford and lead EMEA private capital analyst Nalin Patel offered their “first look” observations about the Venture Monitor report for Q2 2024.

They noted that on the global level, inflation, interest rates, and macro uncertainty have pulled down VC dealmaking.

“Though deal value has seen an uptick due to several large, outsized deals, the dealmaking environment overall is struggling along,” Sanford and Patel said. “The high number of VC-backed companies globally are under pressure from the lower available capital, and many companies are being forced back into the market to raise further private funds because exits cannot be achieved.”

Lil Snack & GamesBeat

GamesBeat is excited to partner with Lil Snack to have customized games just for our audience! We know as gamers ourselves, this is an exciting way to engage through play with the GamesBeat content you have already come to love. Start playing games now!

Fundraising figures are particularly slow, pacing the year for the lowest total commitments since 2015. The slowdown is exacerbated by the high rate of recommitments to the strategy that global LPs realized over the past few years, as investors (particularly in 2021 and early 2022) came back raise a new fund at a much quicker pace. Now that distributions have slowed, many limited partners are facing the inability to reup commitments back of their unbalanced portfolios.

Missing from the global venture market is the middle and large-sized merger and acquisition (M&A) deals. Acquisition counts have remained relatively high, though a large majority of the deals have been small.

The market is fertile ground for tech roll-ups and discount bargains, but larger deals have been balked at due to the need for immediate impact on the acquirers bottom line, which many acquisitions are unable to provide.

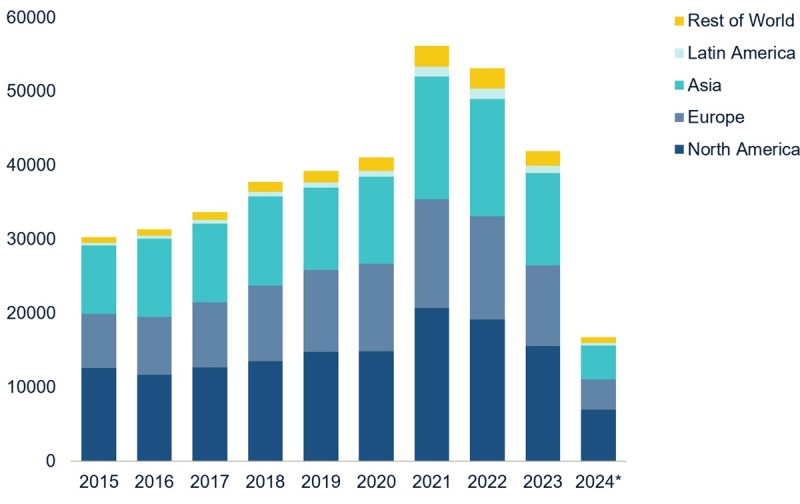

Dealmaking in Latin America is on a slow pace for the year, likely leading to the slowest year of dealmaking since 2018. Wariness caused by the high number of deals in 2021 and 2022 that have led to few exits, as well as the pullback of US investors from the market has led to the slow market.

Latin America exits are on the same pace by count as in 2023, which was the slowest year for exits since 2018, and have generated less than $36 million in value through the first half of the year. If the pace holds, it would be the lowest year for LatAm exit value since 2016.

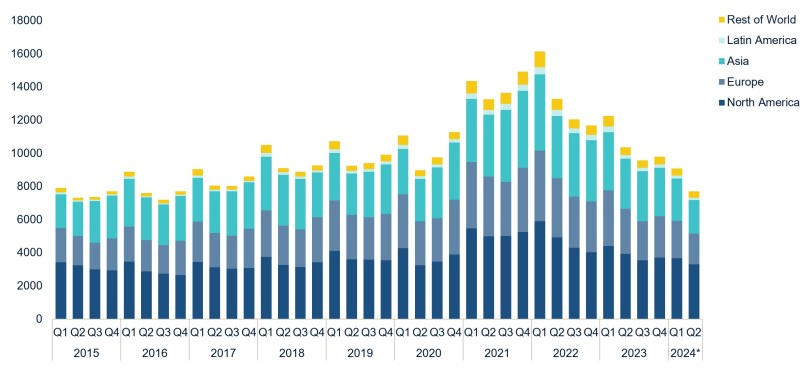

U.S. deal activity has picked up

U.S. deal activity has increased on a count basis for each of the past three quarters. It’s a positive sign that deals are getting done, but lengthening exit slowdown is pressuring companies back into a market that is less forgiving than that which companies are used to, said Patel and Sanford.

Relatively lower deal value growth (QoQ growth this quarter was driven by CoreWeave and xAI deals), highlights the lesser capital availability in the market.

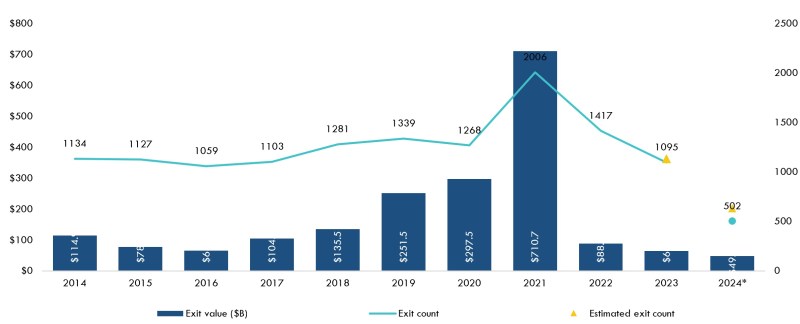

Exits remain elusive. The uptick in exit activity was driven by small deals. Just $23.6 billion in exit value was generated in Q2, less than in Q1. The IPO market has faltered in its restart, despite two high profile IPOs in the first month of the quarter.

For VC returns to see an increase, large tech companies must begin to list publicly at a higher pace than seen through the first half of the year. Exit value is pacing better than both 2022 and 2023, yet outside of those years, the market is facing its lowest exit total since 2016.

U.S. fundraising shows the impact of the lengthened slowdown, with just $37.4 billion in commitments through the first half of the year. The totals have been led by large, name-brand firms. Of that total, more than $7 billion was raised by Andreessen Horowitz, another $3 billion by both Norwest Venture Partners and TCV. Billion-dollar funds have been raised, but potentially at the expense of smaller, emerging managers.

Europe is resilient

Q2 European VC deal activity was resilient and in line with recent quarterly figures with an uptick in deal value despite fewer deals.

Looking at the first half of 2024, European VC deal activity was down slightly on the pace set in 2023. The mixed picture is reflective of the current dealmaking environment. Deals continue to close despite volatile macroeconomic indicators and uncertainty around geopolitics across the continent.

Exit activity in Europe was thin in Q2 and fell further from depressed levels in Q1 2024. If kept up, the pace set in H1 2024 could result in a decade-low for exit value at the year’s conclusion.

Despite rallies in public equities, the lack of exits is attributable to several unconducive factors. For example, previously VC-backed companies that have gone public in recent years have displayed weak growth. Moreover, current appetite to exit has been hampered by ambiguity surrounding realistic market valuations. Investors still await a rebound which is yet to materialize, Pitchbook and NVCA said.

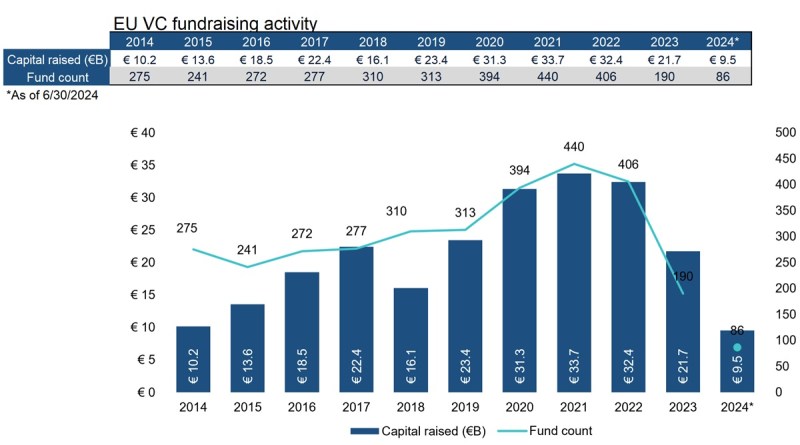

European VC fundraising was solid in the first half albeit pacing slightly down from the levels witnessed in 2023. Fundraising has slowed since 2021 as tougher conditions have emerged for GPs and LPs. fundraising tends to be lumpy across VC ecosystems and underpinned by large fund families managed by established names. In H1, Accel and Creandum closed major funds to help boost figures in Europe.